If you’re thinking about buying a home or need to renew or refinance, one of the first things you'll likely stress about is your credit score — and whether it's good enough to secure a great mortgage rate.

Where your score lands on a lender’s scale can increase the risk of default, so it's true that a good credit score can open more financial doors and unlock better rate offers with a traditional lender.

But life isn't always rainbows and butterflies, so what if your score lands lower on the scale?

Let's examine the WHAT, HOW, and WHY of mortgage lenders and credit scores.

The WHAT: Credit Score Scale

First, what is a credit score? It’s a number assigned by a Canadian credit bureau based on how well you've managed your bills. Two main bureaus operate in Canada: Equifax Canada and TransUnion, and you can check your score for free.

Credit scores range from 300 to 900 with Equifax and 300 to 850 with TransUnion. A higher score is the goal. Here are the typical labels applied to scores:

- Over 760 – Excellent

- 760-680 – Good

- 680-620 – Adequate

- Under 620 – Below Average

But what do these ranges mean for your mortgage rate?

For a mortgage application, a ‘magic’ score of 680 or more (‘excellent’ and ‘good’ slots) unlocks the best rates with a traditional lender — though other factors, such as income source and employment history, may impact your rate.

As the scale drops below 'good,' your mortgage rate will likely be higher — about 1 to 6% or more, depending on your details and lender.

Most traditional (prime) lenders require a score of at least 680 for a refinance or 660 for a purchase. However, some may allow exceptions down to 600 on applications where other criteria are strong.

Alternative lenders may go down to 500, and private lenders typically only consider your home equity and location when lending. Rates from these lender types (B or C lending) will be higher than those offered by traditional lenders (A lending).

The HOW: How do mortgage lenders get your credit score?

When you ask about getting a mortgage rate or mortgage, a broker or bank rep will typically inform you when they need to do a ‘hard’ credit pull (or it may be in the fine print, depending on the online application you filled out).

- A soft pull doesn't affect your score, such as when you check on your own credit score.

- A hard pull is a full credit inquiry that appears on your credit report when you officially apply for a mortgage or other credit product, which can temporarily lower your score by about 10 points (considered a minimal effect).

Multiple hard pulls (e.g. from shopping for a mortgage with different lenders) within a short enough window may not further ding your credit score, and it should recover in about 3 months.

If you use one mortgage broker to check the lenders for you — your credit is usually pulled once to shop multiple lenders, registered as only one inquiry on your credit file.

The WHY: Why are rates higher with a lower credit score?

It comes down to the increased risk of borrower default that a lender would take on for the mortgage loan.

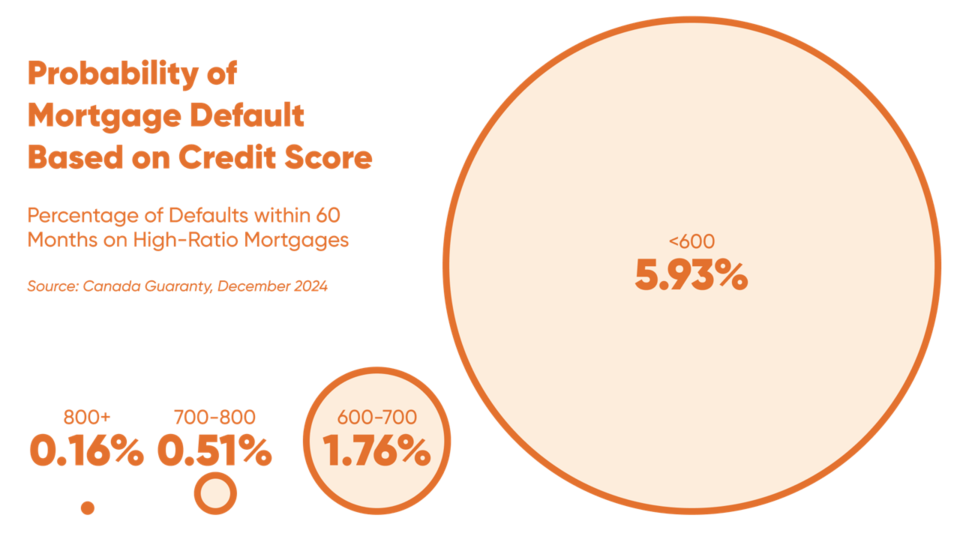

For example, one of Canada's three mortgage default insurance providers, Canada Guaranty, calculates the historical default risk by borrower credit score (for mortgages with less than a 20% down payment), as demonstrated by this graphic:

As you can see, the risk of default rises with each score bracket drop. Below 600, the default potential rises substantially to almost 6% — which is pretty big by lender standards.

That risk doesn't automatically translate into a rate that's 6% higher, but it shows you why it could be.

Your credit score counts. But what can also count? Your home equity.

No matter what number your credit score is, you can apply for a mortgage.

Lower scores can be supported by another factor important to mortgage lenders: home equity.

Whether it's built up from months or years of paying down your mortgage or you're coming in with a larger down payment, a lower LTV (loan-to-value) can help offset your credit score for accessing a better alternative mortgage rate.

That's because home equity offers a mortgage lender more security in getting its money back in the event of default.

Your score, your rate, your best mortgage fit.

You’re not alone if you feel intimidated by a credit score. If your score is already in the 'good' range of 680 or more, you don't need to stress about raising it further just to get a mortgage (unless it helps you stress less, of course!).

The important takeaway here is to be aware of what a lender looks for in a credit score, but it shouldn't define you or prevent you from seeking a good solution.

Wherever your score lands on the scale, friendly mortgage help is available. True North Mortgage has more flexibility than the big banks in finding your best mortgage rate and fit for your situation.

As one of Canada’s top mortgage brokerages, it’s something they’ve been obsessed with for over 18 years — with the industry's best 5-star client review score to prove it.

Anywhere you are in Canada, talk to an expert in your preferred language who cares about saving you (mortgage) cash. Contact Canada's No. 1 Mortgage Broker today.